Refinancing a personal loan allows you to replace your existing loan with a new one, often at a lower interest rate and with reduced monthly repayments. This option may be beneficial if your credit score has improved, as it could enable you to secure a more favourable interest rate.

Key Takeaways

- Potential to Reduce Costs and Payments: Refinancing a personal loan could lower your interest rate and monthly repayments, particularly if your credit score has strengthened.

- May Not Always Be Cost-Effective: In some cases, such as when your loan is nearly paid off or if the new loan includes additional fees, refinancing may add to your overall costs.

- Impact on Credit Score: Refinancing involves a credit check, which can temporarily reduce your credit score. However, making regular payments on the new loan can help improve it over time.

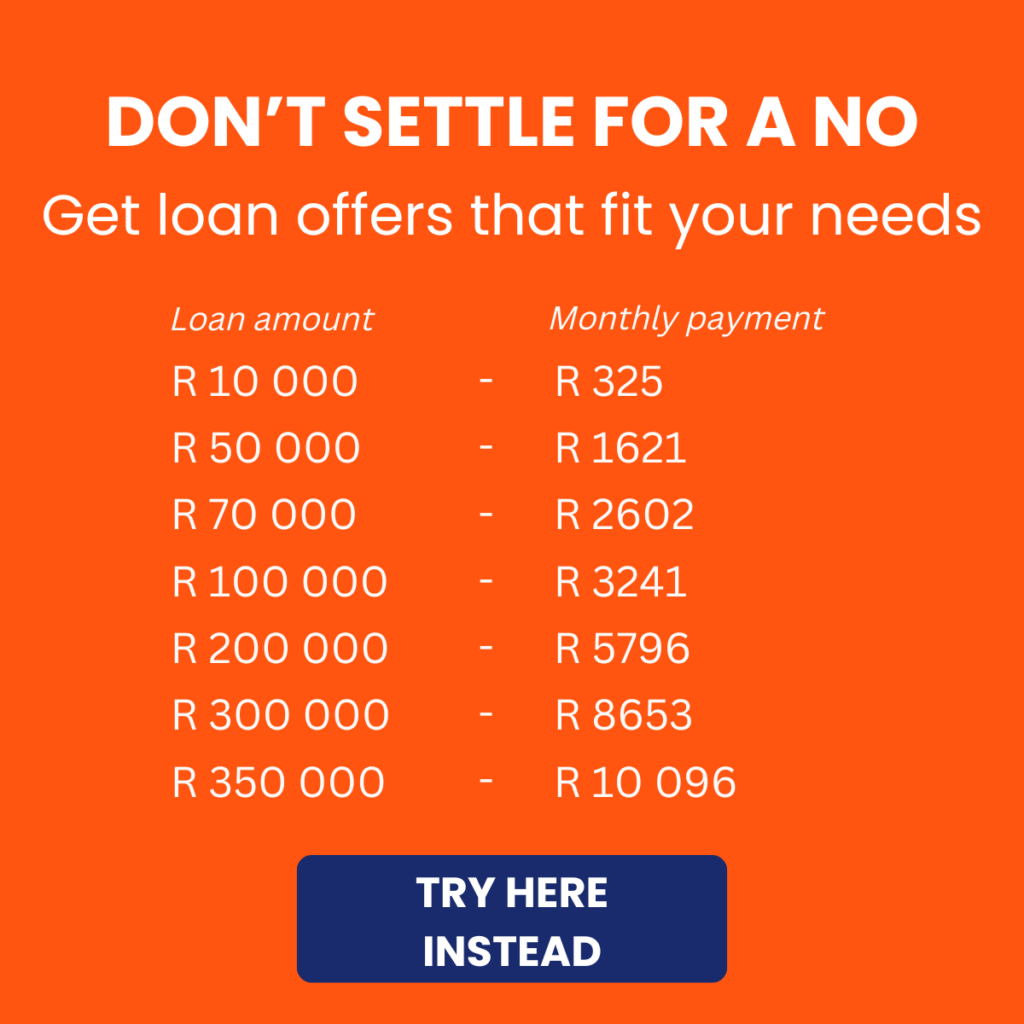

About Arcadia Finance

Secure your loan effortlessly with Arcadia Finance. Enjoy no application fees and select from 19 reputable lenders, each fully compliant with South Africa’s National Credit Regulator standards. Benefit from a streamlined process and trustworthy options tailored to your financial needs.

Refinancing a Personal Loan

Refinancing a personal loan means taking out a new loan, often with a different lender, to settle an existing one. Once the new loan is approved and the refinancing process is complete, the old loan is paid off, and you begin repayments on the new loan instead.

There are various reasons why people opt to refinance. Typically, the main goal is to secure a lower interest rate, which can help reduce overall borrowing costs. In some cases, refinancing may also allow you to access additional funds for a new expense or financial need.

Refinancing can seem complicated, but it doesn’t have to be. Start with a clear understanding by exploring What is refinance debt? and simplify your financial decisions.

How to Refinance a Personal Loan

Refinancing a personal loan requires thorough planning, from calculating the required loan amount and assessing your credit score to comparing offers from different lenders. Once you’ve chosen a lender, the application process is similar to that of a typical personal loan.

Determine the Required Loan Amount

Start by calculating the precise amount needed to settle your existing loan. Knowing the exact payoff amount is essential to find a lender with competitive refinancing terms. This ensures you only borrow what you need, helping you avoid taking on unnecessary debt.

Additionally, check if your current lender charges any prepayment penalties, as these fees can quickly add up and potentially reduce or even cancel out the financial benefits of refinancing.

Review Your Credit Score and Credit Report

Next, check your credit score and report before proceeding with a refinance. This review helps determine if you qualify for a significantly lower interest rate. If the new rate doesn’t offer substantial savings, refinancing may not be worthwhile.

The three main credit bureaus—Equifax, Experian, and TransUnion—provide a free weekly credit report, which allows you to closely monitor your credit status.

When comparing new loans, see if lenders use a soft or hard credit inquiry to provide a quote. Many lenders offer a prequalification option, allowing you to view possible rates with a soft inquiry, which doesn’t immediately impact your credit score.

A hard credit inquiry can temporarily lower your credit score, so it may be best to prioritise lenders that rely only on soft inquiries for initial rate quotes, minimising any potential negative impact on your credit during the refinancing process.

Compare Rates and Terms

Carefully compare rates and terms from multiple lenders before deciding. This helps ensure you secure the most suitable option for your financial needs. Check for fees, including origination fees, which could affect your annual percentage rate (APR). Also, consider the loan amount and terms each lender offers, as these factors play a crucial role in your decision-making.

If your goal is to lower monthly payments, consider whether extending the loan term is truly beneficial. Extending the term, even at a lower APR, may result in paying more interest overall due to the longer repayment period.

Speak with Your Current Lender

While comparing offers, don’t overlook your current lender. Although uncommon, your current lender may provide a better deal for refinancing. With your established relationship, it might also be easier to explore options, including possibly obtaining a second personal loan without needing another credit inquiry.

Apply for the Loan

Once you’ve found a lender with terms that suit you, proceed with the application and gather necessary documents such as your ID number, recent pay slips, bank statements, or tax records. Prequalification is only a preliminary step and not a formal application. To move forward, a full application must be completed, followed by a hard credit check to formally assess your eligibility.

Begin Repaying Your New Loan

After the funds from your new loan are disbursed, use them promptly to settle your previous loan. Acting quickly helps prevent additional interest charges or the risk of managing overlapping loan payments.

With the new loan in place, your repayment phase begins. The start date and repayment terms will be specified in your loan agreement. As with your previous loan, consistent, timely payments are essential to keep your account in good standing.

Refinancing can often serve as a strategic move to consolidate multiple debts into a single manageable loan. Wondering if it’s the right fit for you? Explore the pros and cons of consolidation in Is debt consolidation a good idea? and see how this approach might streamline your financial management.

When You Should Refinance a Personal Loan

Refinancing a personal loan can be advantageous in various situations, particularly if it leads to significant savings or better aligns with your current financial circumstances. Situations Where Refinancing May Be Beneficial:

Improved Credit Score

If your credit score has improved since you took out the original loan, refinancing could help you secure a lower interest rate, potentially lowering your total borrowing costs.

Reduced Income

In cases of income reduction or job loss, refinancing for a longer repayment term might be a helpful strategy. Although this may not reduce the total loan cost, it can lower your monthly payments, providing short-term financial relief.

Goal of Faster Repayment

If you’re now able to make larger monthly payments, refinancing to a shorter loan term can help you pay off the loan sooner, reducing the amount you pay in interest over time.

Ability to Cover Refinancing Fees

Many refinancing loans come with fees, such as origination or application charges, and some lenders may also charge prepayment penalties if you settle the loan early. Factoring in these costs is essential to ensure refinancing is a financially sound choice after accounting for all related fees.

When To Hold Off on Refinancing a Personal Loan

Not every personal loan is worth the time and expense of refinancing. Here are some situations where it may not be practical:

- Small Loan Balance: If only a small amount remains, refinancing might add unnecessary costs through fees or other charges. In these cases, focusing on paying off the remaining balance with your current loan could be more efficient.

- Higher or Similar Interest Rate: When the new loan’s interest rate doesn’t offer savings—or is higher—refinancing might increase costs. This option could be considered only if it’s necessary to lower your monthly payment by extending the loan term.

- Loan Nearing the End of Term: If you’re close to fully repaying your loan, refinancing could add more interest costs. Keeping the existing loan until it’s settled might be the most straightforward and cost-effective choice.

How Refinancing a Personal Loan Affects Your Credit Score

When you refinance a personal loan, a credit check is typically required, which can slightly lower your credit score temporarily. This impact is usually brief, especially if you manage the new loan responsibly by making payments on time.

However, even a minor drop in your score could be important if you’re also planning to buy a car or rent a property soon. Car dealerships and landlords often check credit scores, so refinancing at the wrong time could make it harder to secure a vehicle or accommodation.

Advantages and Disadvantages of Refinancing a Personal Loan

Advantages

- Lower Interest Rate: If interest rates have decreased or your credit score has improved, refinancing may enable you to secure a lower annual percentage rate (APR), resulting in cost savings.

- Quicker Loan Payoff: Refinancing to a shorter loan term can help you pay off your debt faster, provided you can manage higher monthly payments.

- Extended Repayment Period: Lengthening your loan term can reduce monthly payments, making them more manageable. However, this often leads to higher overall interest costs.

- Stable Payments: Transitioning from a variable interest rate to a fixed rate through refinancing can provide predictable monthly payments, enhancing your budgeting.

- Enhanced Credit Score: While the initial credit check for refinancing might cause a slight dip in your score, consistent, on-time payments on the new loan can improve your credit over time.

Disadvantages

- Additional Fees: New loans can come with lender fees, which may diminish any potential savings from refinancing.

- Prepayment Penalties: Some loans charge fees for early repayment. It’s important to check your current loan terms to see if this applies.

- Higher Interest Over Time: Extending the loan term can increase total interest costs, particularly if you’re looking to reduce monthly payments due to financial strain.

- Credit Score Effects: Since refinancing is viewed as a new loan application, it can temporarily lower your credit score, although the impact is typically minimal.

- Time Investment: Finding the right lender, comparing offers, and completing applications can be time-consuming. If your loan is nearly paid off, the effort required for refinancing may not be justified.

Conclusion

Refinancing a personal loan can be an effective financial strategy for South African borrowers looking to lower interest costs, manage monthly payments, or expedite loan repayment. However, it’s crucial to weigh the potential benefits against possible drawbacks, such as additional fees or a temporary decline in your credit score.

Frequently Asked Questions

What does it mean to refinance a personal loan?

Refinancing a personal loan involves replacing your existing loan with a new one, usually to obtain better terms, such as a lower interest rate or modified repayment period. The new loan pays off the old loan, and you make payments according to the new terms.

How can refinancing a personal loan save me money?

You can save money through refinancing by securing a lower interest rate, which reduces the overall cost of borrowing. If your credit score has improved since obtaining the original loan, you may qualify for more favourable rates and terms.

Will refinancing affect my credit score?

Yes, refinancing can temporarily impact your credit score. A credit inquiry is typically part of the refinancing application process, which may result in a slight, short-term decrease in your score. However, making consistent, on-time payments on the new loan can help improve your score over time.

Are there any costs associated with refinancing a personal loan?

Yes, refinancing may incur additional costs, including lender fees, origination fees, and potential prepayment penalties on your original loan. It’s essential to evaluate these costs to determine if refinancing remains financially advantageous.

When might refinancing a personal loan not be the best choice?

Refinancing may not be the best option if your remaining loan balance is low, if the new interest rate isn’t significantly better, or if your current loan is nearly paid off. In these situations, refinancing could lead to additional costs without substantial savings.