A personal loan serves as a practical financial solution, offering access to funds that enable you to cover significant expenses that may be challenging to pay for in one go. This type of loan can also be beneficial for consolidating multiple debts, simplifying your financial obligations by combining them into a single, manageable monthly repayment. Regardless of your purpose for considering a personal loan, it is essential to ensure that this borrowing option aligns with your specific financial situation, that the repayments fit within your budget, and that you have a clear understanding of how the loan operates.

Key Takeaways

- Personal loans are a flexible financial tool: They can cover significant expenses, consolidate debts, and offer manageable repayment terms, making them a practical choice for a variety of financial needs.

- Lenders assess eligibility: Through factors like age, income, employment stability, and credit score, with higher risks leading to stricter requirements and potentially higher interest rates compared to secured loans.

- Alternatives to personal loans: Credit cards, secured loans, overdraft facilities, and peer-to-peer lending, may be more suitable depending on the borrower’s specific financial needs, repayment capacity, and risk tolerance.

What is a Personal Loan?

A personal loan is a financial product widely available through banks and other lending institutions. These loans are among the most common forms of credit and are typically used to cover significant, one-off expenses or to manage costs that cannot be handled through regular income. Personal loans generally feature lower interest rates compared to credit cards, making them a practical choice for managing urgent financial needs.

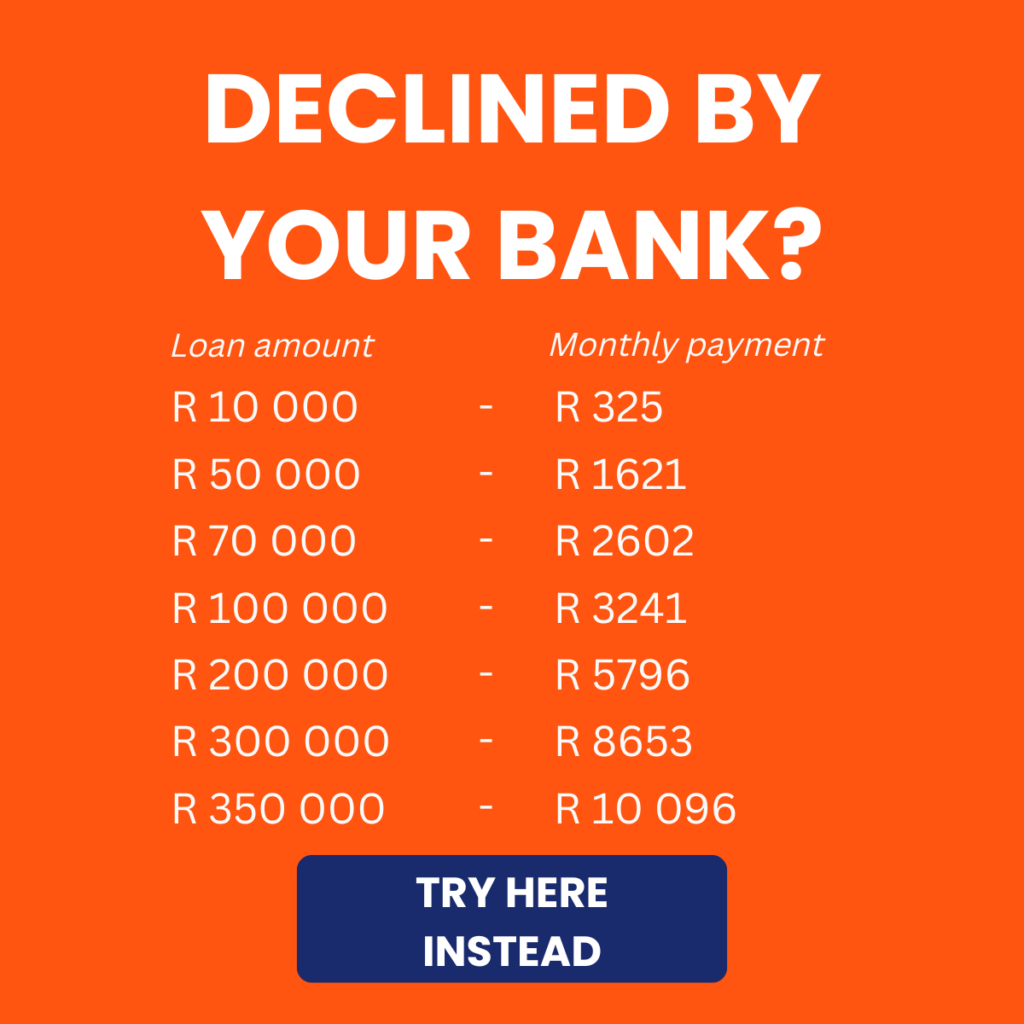

Unlike secured loans, personal loans do not require borrowers to offer assets, such as a car or a home, as collateral. Borrowers can access amounts up to R350 000, with repayment terms ranging from two to five years.

What are the Requirements for Personal Loans?

Personal loans are often utilised to cover a variety of expenses due to their flexibility and the lack of a need for collateral. However, because they are unsecured, they present a higher risk for lenders such as banks and credit institutions. To mitigate these risks, lenders carefully evaluate several factors related to the borrower’s circumstances. These considerations include:

- Age Requirements: Personal loans are typically available to individuals aged between 18 and 60. Borrowers outside this age range may face restrictions or additional conditions when applying for a loan.

- Employment Status: A steady source of income, whether through self-employment or regular salaried work, significantly increases the likelihood of qualifying for a loan. Lenders often favour applicants employed in stable roles within private firms, government organisations, or multinational companies due to the perceived reliability of income from such sources.

- Work Experience: Many lenders stipulate that applicants should have a minimum of two years of total work experience, including at least six months in their current role. This criterion helps lenders assess the stability of the applicant’s employment.

- Minimum Income: The minimum income required to qualify for a personal loan varies between lenders. Borrowers should compare requirements across different institutions to identify the best option for their financial situation.

- Credit Score: A borrower’s credit score, which ranges from 300 to 900, is an important indicator of creditworthiness. A higher score reflects responsible financial behaviour, such as timely repayment of credit card balances and previous loans, while a lower score signals potential risk to lenders.

Meeting a lender’s criteria is the first step in securing a personal loan. But how quickly can your loan application be approved once you check all the boxes? Read our guide How Long Does a Loan Take to Approve? to find out.

About Arcadia Finance

Get your loan with ease through Arcadia Finance! With no application fees and a choice of 19 trusted lenders, all compliant with South Africa’s National Credit Regulator standards, we ensure a seamless process tailored to your financial goals.

The Loan Process

Qualification

To qualify for a loan, three primary factors are evaluated:

- Affordability: This refers to how much you can reasonably repay each month, based on your net income and existing financial obligations.

- Employment Stability: The duration and stability of your employment can affect the amount of credit a lender is willing to provide.

- Credit History: This assesses the risk you may pose to the lender, focusing on your consistency in repaying previous debts and meeting instalment deadlines.

Application

When preparing to apply for a loan, ensure the following steps are completed:

- Identify the loan type you require and contact the appropriate lender.

- Maintain a solid credit score, ideally ranging from 681 to 766.

- Understand the minimum qualifications for the loan you wish to apply for.

- Gather all necessary documentation, including your ID number, proof of income, bank statements, utility bills, employment details, and banking information.

During the application process, the lender will conduct a thorough credit check and evaluate your credit history for any irregularities. Avoid applying for loans on speculation, as multiple applications can negatively affect your credit score.

Loan Approval and Transfer

Loan approval times vary depending on the lender and loan type. This process typically takes between seven days and two weeks, after which the loan amount may be deposited into your account. Some banks process transfers immediately, while others may require up to two business days for the funds to appear.

Repayment

When accepting a loan, you agree to specific repayment terms. It is your responsibility to monitor the repayment schedule, whether the terms involve a single repayment date or recurring monthly instalments. Missing repayments can result in severe consequences, including the loss of secured assets, increased debt, and damage to your credit score.

Account Closure

For some loans, such as home loans, manual account closure or settlement is required. This process involves contacting the credit provider to confirm closure, and they can guide you through the necessary steps to complete this process.

How Are Personal Loans Calculated?

The most significant consideration when determining personal loan eligibility is your ability to repay the loan consistently. To assess this, lenders use two primary methods to calculate the maximum loan amount you may qualify for, both of which are directly tied to your income.

- Fixed Income to Obligation Ratio (FOIR): This method evaluates the portion of your income that is committed to existing financial obligations, including loan repayments and credit card bills. If more than 50% of your income is already allocated to these commitments, your loan application may not be approved.

- Net Monthly Income (NMI) Method: Under this method, the maximum loan amount is determined by applying a multiplier to your net monthly income. Should the calculated eligible amount exceed 30 times your NMI, your loan application is likely to be declined.

Keeping Your Finances on Track

Personal loans can be a useful financial tool when managed carefully, providing support during times of need. They can enhance your financial situation if used wisely. To avoid financial strain, ensure you borrow within your means and seek guidance from a financial advisor if you are unsure about the suitability of a loan.

Advantages and Disadvantages of Personal Loans

Personal loans can be a helpful financial tool in various situations, but they also come with certain limitations. Here is a balanced overview of their advantages and disadvantages to help you decide if this option suits your financial needs.

Advantages of Personal Loans

- Flexibility in Use: Personal loans can be used for a wide range of purposes, from covering unexpected expenses like medical bills to financing significant purchases such as home renovations. This flexibility allows borrowers to address specific financial needs without restrictions on how the funds are used.

- Collateral-Free Borrowing: Unlike secured loans, personal loans do not require any assets, such as a house or vehicle, to be pledged as collateral. This makes personal loans a viable option for individuals without significant assets or those who do not want to risk losing them.

- Fixed Repayment Terms: Most personal loans offer fixed repayment schedules, allowing borrowers to plan their finances with certainty. Knowing exactly how much you will repay each month over a set period can help with budgeting.

- Lower Interest Rates Compared to Credit Cards: Personal loans often come with lower interest rates than credit cards, making them a more cost-effective solution for borrowing, particularly for larger amounts or longer repayment periods.

- Debt Consolidation: Personal loans can simplify financial management by consolidating multiple debts into a single repayment. This approach may reduce the overall interest rate and make repayment more manageable.

Disadvantages of Personal Loans

- Higher Interest Rates Compared to Secured Loans: Since personal loans are unsecured, lenders face greater risks, which often result in higher interest rates than secured loans. Borrowers with lower credit scores may find the rates particularly steep.

- Potential Financial Strain: If not managed responsibly, personal loans can strain your finances. Borrowing more than you can afford to repay or missing payments can lead to increased debt and negatively impact your credit score.

- Fees and Charges: Personal loans often come with additional costs, such as initiation fees, monthly service fees, and penalty fees for late payments or early settlement. These charges can increase the overall cost of the loan.

- Impact on Credit Score: Failing to make repayments on time can significantly damage your credit score, affecting your ability to access credit in the future. Additionally, applying for multiple loans within a short period can lower your score.

- Shorter Repayment Periods: While some borrowers appreciate shorter repayment periods, others may find the higher monthly instalments challenging to manage compared to loans with longer repayment terms.

Alternatives to Personal Loans

Credit Cards

Credit cards are a practical option for managing smaller, short-term expenses. They provide a revolving line of credit that can be used repeatedly up to a specified limit. This option is particularly useful for covering daily purchases or unexpected costs. Credit cards often come with interest-free periods if the balance is repaid in full each month. However, the convenience they offer can lead to overspending, and balances not paid on time are subject to high interest rates, which can increase financial strain.

Secured Loans

Secured loans are ideal for larger expenses or when lower interest rates are a priority. These loans require borrowers to provide collateral, such as a car or property, to secure the loan. This reduces the lender’s risk, often resulting in lower interest rates and the possibility of borrowing larger amounts. While this makes secured loans a cost-effective solution for significant purchases, failure to meet repayment obligations could result in the loss of the pledged asset.

Overdraft Facilities

An overdraft is a flexible borrowing solution linked to a bank account, allowing individuals to withdraw funds beyond their current balance, up to a pre-approved limit. It is commonly used to manage short-term cash flow gaps or emergency expenses. Interest is charged only on the amount utilised, making it a cost-effective option for temporary needs. However, overdraft facilities often carry higher interest rates than personal loans and may lead to dependency if not managed carefully.

Peer-to-Peer (P2P) Lending

Peer-to-peer lending platforms provide a relatively new alternative in South Africa, enabling borrowers to access funds directly from individual investors. This option is particularly useful for those with non-traditional credit profiles who may not qualify for standard loans. P2P lending often offers competitive interest rates and flexible terms, although availability and regulation can vary. Borrowers should carefully review terms and conditions to ensure transparency and suitability.

Choosing the Right Option

When considering financing alternatives, it is essential to evaluate your financial circumstances and the intended use of the funds. For short-term or small-scale needs, options like credit cards or overdrafts may suffice, while secured loans are better suited for significant, long-term expenses. Always assess the associated costs, risks, and repayment terms to determine the most appropriate solution for your situation. If you are uncertain, seeking advice from a financial professional can provide valuable guidance.

Conclusion

Personal loans can be a practical and flexible solution for addressing various financial needs, from covering large expenses to consolidating debt. However, it is essential to evaluate your financial situation, understand the loan terms, and compare alternatives such as credit cards, secured loans, or overdrafts before making a decision. By carefully considering factors like interest rates, repayment periods, and eligibility requirements, you can choose the financing option that best aligns with your budget and financial goals. Responsible borrowing, coupled with a clear repayment plan, can ensure that a personal loan supports your financial stability without creating undue strain.

Frequently Asked Questions

What is the difference between a personal loan and a secured loan?

A personal loan is unsecured, meaning you do not need to provide collateral such as a car or property to qualify. Secured loans, on the other hand, require collateral, which reduces the lender’s risk and often results in lower interest rates. However, with a secured loan, failure to repay could lead to the loss of the pledged asset.

How does my credit score affect my eligibility for a personal loan?

Your credit score is a key factor that lenders consider when assessing your loan application. A higher credit score demonstrates responsible financial behaviour, such as timely repayment of debts, and increases your chances of approval. Conversely, a lower score may lead to higher interest rates or rejection of your application.

Can I use a personal loan to consolidate debt?

Yes, personal loans are commonly used for debt consolidation. By combining multiple debts into one loan with a single monthly repayment, you can simplify financial management and potentially reduce your overall interest rate, depending on the terms of the loan.

What happens if I miss a repayment on a personal loan?

Missing a repayment can result in penalties, increased interest, and potential damage to your credit score. Repeated missed payments may lead to legal action by the lender. If you are struggling to make repayments, it is advisable to contact your lender immediately to discuss possible solutions.

Are there hidden fees associated with personal loans?

Personal loans may come with additional costs such as initiation fees, monthly service fees, and penalty fees for late payments or early settlement. It is important to review the loan agreement thoroughly and clarify any charges with the lender before signing.