Want a Revolving Loan? Qualify Fast!

Why wait to take charge of your finances? Dive into the benefits of revolving loans and see how they can adapt to your changing financial goals.

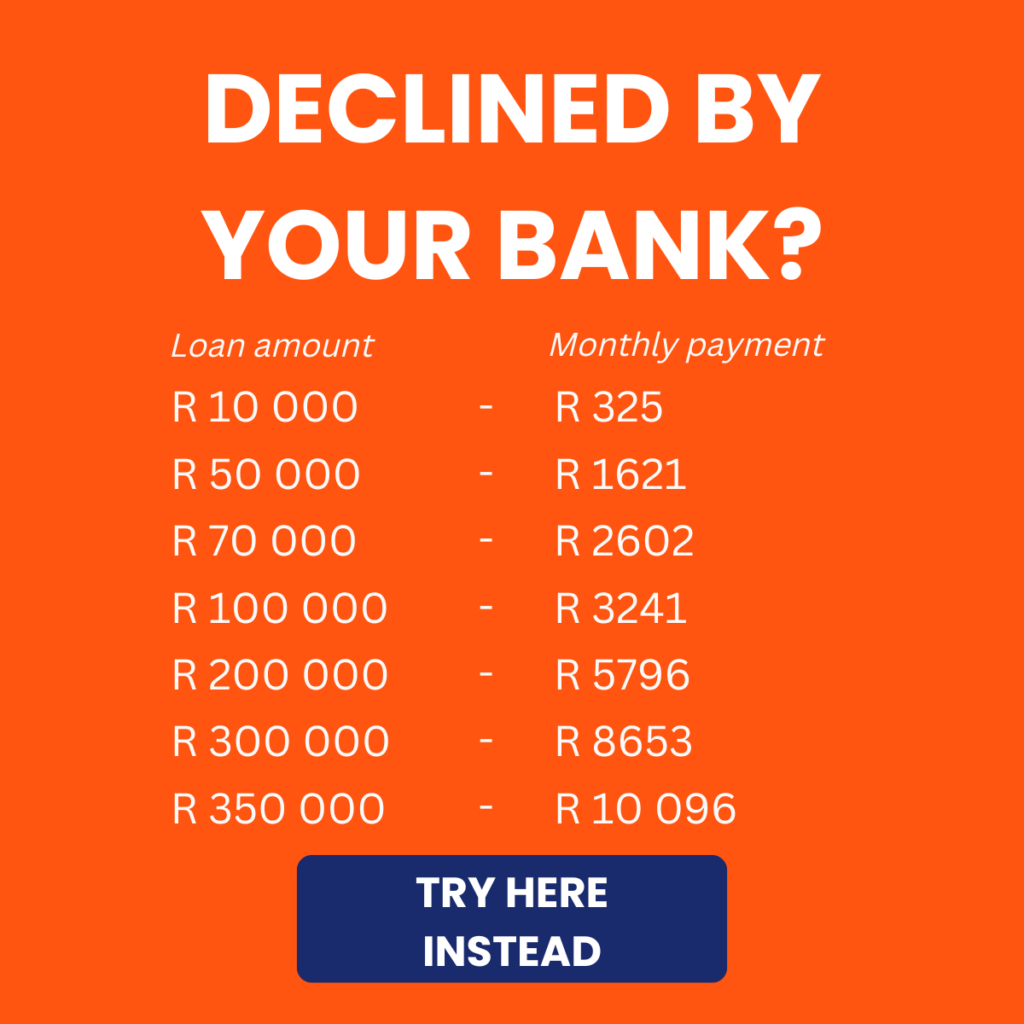

Arcadia Finance helps you in the search of loans from different banks and lenders. Fill in a free application and get loan offers from up to 16 lenders. We work with well-known, trusted, and NCR-licensed lenders in South Africa.

Selecting an appropriate credit solution requires a clear understanding of your specific needs and expectations from the credit facility. A revolving loan is one possible option, offering greater flexibility in accessing funds. However, it is a type of loan that demands thoughtful and consistent management to ensure it remains beneficial and aligns with your financial goals.

What is a Revolving Loan?

A revolving loan is a credit option that offers flexibility in managing repayments and withdrawals as needed. Unlike traditional loans, it allows for:

- Additional repayments at any time: This feature enables you to reduce the outstanding balance at your convenience.

- The ability to borrow repaid amounts again without reapplying: Once a specified portion of the loan (often around 15%) has been repaid, you can access those funds again. This arrangement is beneficial for addressing unexpected expenses.

A revolving loan facility is commonly used by both public and private businesses as a flexible credit line that can adapt to changing financial needs over time. This type of credit is known as a variable line, meaning the interest rate can change depending on market conditions. If interest rates increase in broader credit markets, the lending bank may also raise the rate on this facility. Revolving loan rates tend to be higher than standard loan rates and typically fluctuate with the prime rate or similar indicators. Financial institutions also generally charge a fee to set up this type of loan.

To determine loan approval, lenders assess several factors, including the company’s stage, size, and industry. They review financial statements such as the income statement, cash flow statement, and balance sheet to evaluate the company’s ability to repay. Businesses demonstrating steady income, solid cash reserves, and a good credit rating often have better chances of approval. The balance on a revolving loan can vary from zero up to the maximum approved limit, depending on the company’s financial situation and needs.

About Arcadia Finance

Effortlessly secure your loan with Arcadia Finance. Enjoy zero application fees and choose from 16 trusted lenders, all compliant with South Africa’s National Credit Regulator. Simplify your loan process with financial options you can trust.

How Does a Revolving Loan Work?

A revolving loan offers a continuous line of credit that you can access as long as you meet the minimum repayment obligations. With each payment you make, your available credit increases, allowing you to reuse the funds as needed. This structure is akin to a savings account: the more you borrow, the less available credit you have, while regular payments replenish the credit at your disposal. This flexibility can be especially beneficial for managing unexpected expenses, providing quick access to funds when required.

Revolving Loan Eligibility Requirements

To qualify for a revolving loan in South Africa, applicants—whether individuals or businesses—must meet specific financial and documentation criteria. These requirements help ensure that borrowers can responsibly manage the flexibility that a revolving loan provides.

Individual Eligibility Factors

- Credit Score: A credit score of 600 or higher is generally preferred, indicating a reliable credit history.

- Income Proof: Applicants must demonstrate a stable income through payslips or bank statements to show they can manage ongoing repayments.

- Debt-to-Income Ratio: A manageable level of existing debt compared to income strengthens the application.

- Employment Stability: Consistent employment is advantageous; self-employed individuals may need to provide additional proof of income.

- Required Documents: Typically, you will need a valid ID, proof of residence, income documentation, and a recent credit report.

Business Eligibility Factors

- Financial Statements: Businesses must provide an income statement, cash flow statement, and balance sheet to showcase revenue and financial stability.

- Credit Rating: A positive business credit history enhances approval chances.

- Operational History: Lenders prefer companies with at least one to three years of operation.

- Industry Considerations: Certain industries may face stricter evaluation.

- Required Documents: Standard requirements include company registration papers, audited financial statements, tax compliance certification, bank statements, and proof of business address.

While meeting these criteria can enhance your application, it does not guarantee approval, as each application undergoes a thorough review. Being well-prepared with the necessary documents and understanding these requirements can significantly improve your chances of securing a revolving loan that fits your financial needs.

Advantages and Disadvantages of Revolving Loans

Advantages

- Ongoing Access to Credit: You can repeatedly use the funds without needing to reapply, provided repayments are made on time.

- Flexible Usage: Funds can be allocated to any purpose, allowing for greater freedom in managing financial needs.

- Convenience of Repayment Options: Borrowers can choose flexible repayment terms that can be adjusted based on their financial situation, offering a more manageable way to pay back the borrowed funds.

Disadvantages

- Risk of Accumulating Debt: If a revolving loan is mismanaged, it can lead to high debt levels that may become challenging to control, potentially negatively impacting your credit score.

- Higher Interest Rates: These loans typically carry higher interest rates, making them more expensive compared to other credit options.

- Account Restrictions on Late Payments: Missing payments may result in the lender restricting access to the account, which could limit available credit and increase repayment obligations.

Consult with an Accredited Financial Advisor

Accessing credit is crucial for many individuals looking to achieve their personal or financial goals. Your unique needs, financial situation, and spending habits significantly influence the most appropriate credit solution for you. If you’re contemplating a revolving loan as a viable option, it’s highly advisable to consult a qualified financial advisor. Engaging with a professional prior to making a commitment can help you gain a clear understanding of how this type of loan may fit into your overall financial strategy.

How Does a Revolving Loan Differ from Other Credit Solutions?

A revolving loan operates quite differently from a personal loan. With a personal loan, you borrow a fixed sum of money once, which cannot be borrowed again after repayment begins. The loan is repaid through fixed monthly instalments over a set period, and the interest rate is usually based on your credit rating.

In contrast, a revolving loan functions more like a credit card or an overdraft facility, allowing you to access funds multiple times, provided you meet the repayment requirements. This continuous access can be ideal if you prefer ongoing flexibility in borrowing. However, if your need is for a single lump sum for a specific expense, a personal loan may be more suitable.

Comparing Revolving Loans with Overdraft Facilities

| Feature | Revolving Loan | Overdraft Facility |

|---|---|---|

| Purpose | Suitable for ongoing, flexible access to credit for varied expenses, often larger in scale | Primarily for short-term or emergency needs, covering unexpected expenses or temporary cash shortfalls |

| Interest Rates | Typically variable, often higher than standard loans but may fluctuate with market rates | Usually higher than revolving loans, often charged daily on outstanding balance |

| Borrowing Limits | Fixed limit set at the time of approval, which can be re-borrowed once repaid | Limit generally based on a percentage of the account holder’s monthly income or credit history |

| Repayment Structure | Flexible repayments; credit becomes available again as amounts are repaid | Flexible but requires minimum monthly repayments to avoid penalties; no fixed term |

| Fees and Charges | Setup fees and monthly maintenance fees are common; charges may apply for withdrawals | Monthly or annual fees often apply; may include penalty fees for excessive use or missed payments |

| Access to Funds | Funds can be accessed repeatedly up to the approved limit, similar to a line of credit | Funds are available up to the overdraft limit, with automatic access when the account balance is low |

| Ideal Use Case | Suitable for ongoing projects or variable expenses requiring adaptable credit access | Best for occasional, short-term needs where quick access to funds is essential |

Alternatives to Revolving Loans

If you’re uncertain about whether a revolving loan is the right choice, consider other credit options that may better align with your financial goals:

Term Loans

Term loans provide a fixed loan amount with scheduled repayments over a specific period. They are ideal for significant, one-time expenses such as purchasing a car or funding home improvements. With structured terms and typically lower interest rates, term loans offer borrowers predictable costs and a clear repayment timeline.

Credit Cards

Credit cards offer flexible access to funds, akin to revolving loans, but they are generally better suited for smaller, ongoing purchases or managing daily expenses. While convenient, credit cards often come with high-interest rates, making it crucial to pay off balances regularly to avoid accumulating debt.

Personal Loans

Personal loans provide a lump sum with fixed repayments, usually over a period of two to five years. They are well-suited for one-time expenses, such as medical bills or debt consolidation, offering a structured repayment plan and typically lower rates than credit cards.

Risks and Limitations of Revolving Loans

Revolving loans provide flexible credit access, but they come with specific risks that borrowers should be aware of:

- Accumulating High-Interest Debt: Due to their generally higher interest rates, revolving loans can lead to debt accumulation if only minimum payments are made. It’s crucial to make regular repayments to avoid an increasing balance and higher interest costs.

- Variable Interest Rates: Many revolving loans feature variable interest rates, which means repayments can rise with market fluctuations. This risk should be considered, especially for borrowers on fixed budgets.

- Self-Regulation of Repayments: Revolving loans depend on disciplined repayment habits. Without consistent payments, borrowers may face prolonged debt and escalating costs.

- Credit Score Impact: Poor management, such as late payments or maintaining high balances, can negatively impact your credit score, limiting future borrowing opportunities.

- Fees and Penalties: Additional costs associated with setup, maintenance, and missed payments can make revolving loans more expensive. Understanding all potential fees is essential to avoid unexpected expenses.

Conclusion

Revolving loans can be a beneficial credit option for both individuals and businesses that require flexible access to funds, particularly for variable or recurring expenses. However, their effectiveness as a financial tool relies heavily on careful management. With potentially higher interest rates and variable terms, it is crucial for borrowers to maintain discipline by making regular payments and avoiding excessive debt accumulation to prevent long-term financial strain.

Frequently Asked Questions

A revolving loan is a flexible credit line that allows you to borrow, repay, and borrow again up to a set limit without the need to reapply. As you make repayments, your available credit is replenished, enabling continuous access to funds. This type of loan is useful for managing variable or unexpected expenses but requires disciplined repayment to avoid accumulating debt.

Unlike a personal loan, which provides a fixed amount with set repayments over a specific period, a revolving loan allows you to access funds multiple times as long as you meet repayment requirements. While personal loans are best suited for one-time expenses, revolving loans are ideal for ongoing or unpredictable needs, offering greater flexibility in usage.

Revolving loans carry several risks, including the potential for accumulating high-interest debt due to generally higher rates. Many of these loans have variable interest rates, meaning costs can increase if market rates rise. Additionally, since repayments aren’t fixed, borrowers must manage their debt carefully to avoid prolonged debt and negative impacts on their credit scores.

Yes, revolving loans typically include various fees, such as initiation or setup fees, monthly maintenance fees, and potentially penalties for missed payments. Understanding all applicable fees is crucial to avoid unexpected costs and accurately assess the loan’s overall affordability.

Eligibility for a revolving loan depends on several factors, including credit score, income stability, and current debt levels. Lenders review these factors to assess a borrower’s ability to manage the flexible nature of revolving credit. Businesses may also need to provide financial statements and demonstrate a positive credit history for approval.