Purchasing a vehicle is a significant decision. With an array of car loan options available, it can be challenging to determine the right choice. However, selecting the ideal car finance provider when acquiring your desired car can greatly impact your overall experience.

Key Takeaways

- Car Finance Options: South African banks like Standard Bank, WesBank, Absa, and First National Bank (FNB) offer tailored vehicle finance solutions, including instalment sales, leases, and private or dealership finance, with varying income and vehicle requirements.

- Interest Rates and Loan Terms: Interest rates can be fixed or variable, influenced by credit scores, loan duration, deposit contributions, and balloon payments. Loan terms impact monthly payments, with shorter terms increasing instalments but reducing total interest.

- Additional Costs and Considerations: Deposits, financial buffers, fees, vehicle insurance, and balloon payments all play a crucial role in determining the overall cost and manageability of car finance agreements.

About Arcadia Finance

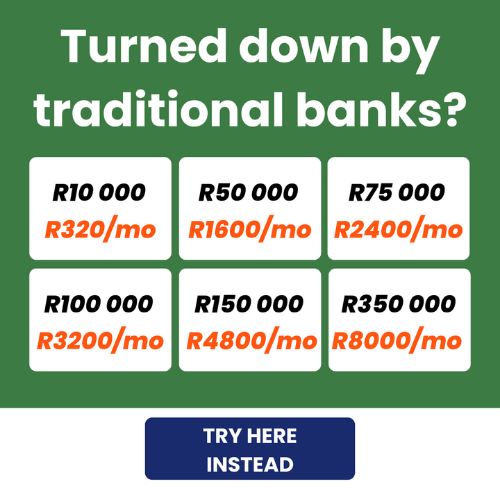

Arcadia Finance makes securing your loan simple and reliable. Choose from 19 respected lenders, all compliant with South Africa’s National Credit Regulator, and enjoy no application fees. Tailored options and a seamless process designed for your peace of mind.

What is Car Finance?

Vehicle finance refers to obtaining a loan specifically for purchasing a car. This is a form of secured borrowing where the loan is tied to the vehicle being purchased, either from a private seller or a dealership. These loans are designed exclusively for vehicle purchases and cannot be used for any other purpose. Car finance options are generally provided by banks, financial institutions, or specialised alternative lenders offering this product. Many people opt for car finance to avoid the significant upfront cost of buying a vehicle outright, allowing them to own a car while spreading payments over manageable monthly instalments. For South Africans, this arrangement often helps preserve savings for other important investments, such as purchasing property.

How Are Vehicle Finance Interest Rates Calculated?

The interest rate for your car loan may be set as either fixed or variable. Fixed rates provide stability, while variable rates fluctuate based on economic conditions, such as changes in the repo rate. These variations influence the total cost of the loan over time:

- Loan Term Duration: This refers to the length of time over which the loan repayments are scheduled.

- Loan Amount: The total amount borrowed, which is based on the price of the vehicle, including any additional features or costs.

- Deposit Contribution: Whether a deposit has been made, and if so, the amount of that deposit.

- Credit Rating: Your credit score, which reflects your financial behaviour, including spending patterns and repayment history for previous loans.

Car payments can often feel overwhelming, but you can reduce them significantly by following the 7 best strategies to lower your car payments in South Africa. Whether it’s through refinancing, budgeting, or negotiating with your lender, these actionable tips can make a world of difference to your monthly finances

The Various Types of Car Finance

When considering car finance, the first step is deciding where you intend to purchase the vehicle. There are two primary types of car finance available, each suited to different purchasing situations.

Dealership Finance

This option applies when buying a vehicle from a dealership, whether it is new or pre-owned. Dealership finance is designed to provide you with the appropriate financial protection required for this specific purchase scenario.

Private Vehicle Finance

Private vehicle finance is tailored for situations where the vehicle is being purchased directly from a private individual.

Within these two categories of car finance, the specific terms and conditions will be determined by the financial institution providing the funding. Typically, the agreements made with the lender fall into one of the following formats:

- Instalment sale agreements, where payments are made in instalments over an agreed period until the vehicle is fully paid off.

- Lease agreements, which involve the payment of periodic instalments for the use of the vehicle without immediate ownership.

When exploring car financing options, it’s essential to understand all available alternatives. If traditional bank loans don’t suit your needs, consider learning more about how rent-to-own cars work and why they might be a better fit for your financial situation.

The Best Car Finance Providers in South Africa

Standard Bank Vehicle Finance

Standard Bank offers vehicle finance through two primary options: instalment sales and leasing. With an instalment sale, you can purchase your desired vehicle and repay the cost in regular instalments over a term agreed upon by both you and the bank. Before approving a car loan, Standard Bank conducts a comprehensive credit assessment. To qualify for vehicle finance or a lease, you must have a minimum monthly income of R5 000. The repayment term can extend up to 84 months.

To determine what you can afford, Standard Bank provides three different vehicle finance calculators: affordability, purchase price, and monthly repayments. These tools can help you make an informed decision about your vehicle financing needs.

WesBank Vehicle Finance

WesBank simplifies the vehicle finance process with a clear guide and a user-friendly mobile app, making car purchases more straightforward for South African customers. The bank requires a minimum income of R7 500 per month to qualify for financing. One standout feature of WesBank is its W-shop, a convenient platform where customers can purchase tyres, windscreen wipers, and even personalised number plates. WesBank also provides financing for vehicles priced at R30 000 or more. Their vehicle finance calculator is easy to use, offering quick insights into the affordability of your desired car.

Absa Vehicle Finance

Absa Vehicle Finance helps you secure your ideal car with ease. They offer competitive interest rates starting at 9.25% and repayment terms ranging from 24 to 72 months. Customers can reduce their monthly instalments by opting for a deposit or a balloon payment. Additionally, Absa allows early settlement of vehicle loans without penalties if the outstanding amount is below R250 000. As vehicle insurance is mandatory for financed cars in South Africa, Absa has partnered with insurers to provide in-house options for added convenience. To determine your affordability, you can use the Absa vehicle finance calculator.

FNB Vehicle Finance

First National Bank (FNB) offers a range of vehicle finance options to suit your needs, whether you are looking to drive a car, ride a motorbike, or even invest in a leisure vehicle. FNB provides three distinct financing options: dealership finance, private vehicle finance, and leisure vehicle finance. With dealership finance, you can purchase a vehicle from a dealership, provided it is no older than 10 years. To qualify, you need to be permanently employed with a minimum monthly income of R6 000, and the vehicle’s value must be more than R30 000 after placing a deposit. For those seeking private vehicle finance, FNB makes it possible to purchase a vehicle from a private seller, with the car’s age extending up to 20 years. The income requirements remain the same at R6 000 per month.

Leisure vehicle finance is available for recreational purchases, such as motorbikes, caravans, or vintage convertibles, provided they are bought from an authorised dealership. In the case of caravans, they must not be older than 20 years. To assist in planning your repayments, FNB provides a vehicle finance calculator, enabling you to estimate your monthly costs before committing to a purchase.

Why You Should Consider Financing a Car

Many South Africans aspire to buy a car with cash, but this is not always practical, making car financing a more suitable option in many cases. Opting for a car loan allows you to preserve your savings for investments in assets that can appreciate, such as property or shares, enabling you to focus on wealth building while meeting transportation needs. Additionally, financing a car and making regular, timely repayments helps establish a good credit history, improving your chances of securing future loans and better financial opportunities. For those looking to rebuild their credit score, consistent car finance repayments can be an effective strategy. Moreover, car finance offers the flexibility to borrow up to 100% of the vehicle’s value, allowing you to purchase your desired car without needing an upfront deposit.

Beyond securing car finance, understanding the different types of car insurances in South Africa is critical to protecting your investment. From comprehensive cover to third-party liability, ensuring you choose the right option can save you from unexpected costs.

What To Consider Before Taking Out A Car Loan

Interest Rates on Car Loans

Typically, the better your credit history, the more favourable the interest rate you may receive. In most cases, the interest rate is calculated as a percentage above the prime lending rate, and combined with the deposit you provide, it impacts the affordability of your monthly instalments.

A variable interest rate aligns with changes in the repo rate, meaning your repayments may fluctuate. On the other hand, a fixed interest rate offers stability but may come with a slightly higher rate, as lenders factor in potential changes to the repo rate over the term of the loan.

Loan Repayment Terms

The loan repayment term refers to the total duration over which you repay the loan, typically calculated in years. Shorter loan terms result in higher monthly repayments, as the total amount must be settled over a shorter period. Longer terms, however, spread the repayments over a greater timeframe, choosing a longer repayment term can lower your monthly instalments but may lead to paying more in total interest across the lifespan of the loan.

Deposit

While there is no legal obligation to provide a deposit for vehicle finance under the National Credit Act, it is generally considered a smart financial decision. A deposit, often at least 10% of the vehicle’s cost, can significantly lower your monthly repayment amount and shorten the loan term. Larger deposits typically lead to reduced borrowing costs and more manageable financial commitments.

Financial Buffer

It is prudent to maintain a financial buffer beyond your disposable income to cover loan repayments. Falling behind on payments can negatively affect your credit score, resulting in higher interest rates for future loans and potentially creating financial strain. Maintaining a buffer can help you manage unexpected expenses and keep your repayments on track.

Additional Fees

Be mindful of any fees associated with purchasing a vehicle, such as administrative charges or ownership transfer costs. Understanding these expenses upfront will help you budget effectively and avoid surprises during the buying process.

Vehicle Type

This is especially relevant when buying second-hand vehicles but is also worth considering for new purchases. Inspect the vehicle thoroughly, including its interior, exterior, and engine, to ensure it is in good condition. Personal confirmation of the vehicle’s condition can save you from unexpected repair costs later. For a fee, you can also get the vehicle inspected by the Automobile Association – they will then issue a comprehensive report on its fitness for purpose.

Vehicle Insurance

Dealerships and Banks typically require you to have insurance before driving a new vehicle off their premises. This is because both the dealership and the financing institution share the financial risk of the purchase. Adequate insurance coverage ensures protection against risks that could affect the vehicle’s value or your ability to repay the loan.

Balloon Payments or Residual Purchase Agreements

A balloon payment option allows you to finance only a portion of the vehicle’s cost, with the remaining balance due at the end of the loan term. This amount, usually between 15% and 35%, is influenced by factors such as the vehicle’s age. While this option can reduce monthly repayments, it requires a significant lump sum payment at the end to secure ownership of the vehicle.

Conclusion

Selecting the right car finance option in South Africa requires careful consideration of various factors, such as interest rates, loan terms, deposit contributions, and additional fees. Whether you choose dealership or private finance, understanding the terms and conditions of each provider is essential to making an informed decision. Banks like Standard Bank, WesBank, Absa, and FNB offer diverse vehicle finance solutions tailored to different needs. By comparing these options and considering your financial situation, you can secure a car finance deal that fits your budget while maintaining long-term financial stability.

Frequently Asked Questions

What is the minimum income requirement for car finance in South Africa?

The minimum income requirement varies by bank. For example, Standard Bank requires a monthly income of R5 000, WesBank R7 500, and FNB R6 000. Always check specific requirements with your chosen lender.

Is it mandatory to pay a deposit when applying for car finance?

No, paying a deposit is not mandatory under the National Credit Act. However, providing a deposit can significantly lower monthly repayments and reduce the overall loan term.

What is the difference between fixed and variable interest rates?

Fixed interest rates remain constant throughout the loan term, offering payment stability, while variable rates fluctuate with changes in the repo rate, potentially impacting monthly repayments.

Can I finance a vehicle from a private seller?

Yes, banks such as FNB and other lenders offer private vehicle finance, allowing you to purchase a car directly from a private individual under specific conditions, such as the car’s age and value.

What happens if I cannot make my car loan repayments?

Missing repayments can negatively affect your credit score and may lead to penalties or repossession of the vehicle. It’s crucial to budget appropriately and maintain a financial buffer to avoid defaulting on payments

Fast, uncomplicated, and trustworthy loan comparisons

At Arcadia Finance, you can compare loan offers from multiple lenders with no obligation and free of charge. Get a clear overview of your options and choose the best deal for you.

Fill out our form today to easily compare interest rates from 19 banks and find the right loan for you.