Your loan application has just been rejected—what should you do next? Before making any immediate decisions, take a step back and evaluate the situation carefully. Start by determining the specific reason for the denial and identifying the exact stage in the application process where the rejection occurred. Understanding these details will help you decide on the most appropriate course of action.

Key Takeaways

- Understanding Why Your Loan Was Rejected: If your bank declined your loan application, the first step is to determine the specific reason. Common factors include low credit scores, insufficient income, high debt-to-income ratios, or missing documentation.

- Benefits of Online Lenders Compared to Traditional Banks: Online lenders provide faster loan approvals, more flexible requirements, and fully digital application processes, making them a viable alternative for borrowers who struggle to meet strict bank criteria. However, comparing lenders is essential to find the most competitive rates and terms.

- Choosing the Right Online Loan Provider in South Africa: With multiple online lenders available, borrowers should compare options based on loan amounts, repayment terms, interest rates, and eligibility criteria.

Why Your Bank Loan Application Might Be Declined

There are multiple factors that could lead to a loan application being unsuccessful. To understand why your application was rejected, it is advisable to contact the lender directly or review your credit report. You are entitled to obtain a free credit report once per year, which provides a detailed breakdown of your credit status and financial history. Below are some common reasons why lenders may decline loan applications:

Limited or No Credit History

If you have never borrowed money, taken out a loan, or owned a credit card, your credit profile may be nonexistent. Lenders assess risk based on your borrowing history, and without a credit track record, they may be hesitant to approve your loan. If you do have existing credit, ensure that you check your credit score before applying. A low credit score can indicate missed payments, frequent loan applications, or other financial behaviours that make you appear as a high-risk borrower.

Insufficient Income

Lenders require proof that you earn enough to meet the monthly repayment obligations for the loan amount requested. If your income is too low or inconsistent, they may view your financial position as inadequate to handle additional debt. Before applying, it is essential to assess how much income is required for the loan type and amount you are seeking.

High Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) measures how much of your earnings are already allocated towards existing debt repayments. A DTI exceeding 30% is typically considered unfavourable, as it suggests that a significant portion of your income is already committed to repaying other loans or financial obligations. A high DTI signals to lenders that you may struggle to manage additional debt. To improve your chances of approval, you may need to reduce existing debt or increase your income before applying for a new loan.

Errors on Your Credit Report

Although uncommon, inaccuracies in your credit report—such as fraudulent activity, identity theft, or inaccurate reporting from a previous lender—can negatively affect your loan applications. These errors can remain on your record for some time, leading to unwarranted rejections. If you suspect an issue, it is important to dispute errors with the credit bureau and rectify discrepancies before applying for a loan.

Incomplete or Incorrect Documentation

Failing to submit all required documents or providing inaccurate information can result in an automatic rejection of your application. Lenders have strict criteria for verifying financial and personal details. To avoid unnecessary delays or denials, ensure that you review the application checklist carefully and submit all necessary paperwork in the correct format.

Understanding what banks check when applying for a loan can help you pinpoint why your application was declined. From your credit score to your income stability, banks are strict gatekeepers — but online lenders are often more flexible.

About Arcadia Finance

Get your loan with ease through Arcadia Finance. There are no application fees, and you can choose from 19 trusted lenders, all registered with South Africa’s National Credit Regulator. Experience a smooth, reliable process designed to suit your financial goals.

The Fundamentals of Online Lending

Online loans are a form of financing that individuals can apply for, manage, and repay entirely via the internet. These lending options include a variety of financial products, such as personal loans, business financing, and short-term payday advances, catering to different borrower needs.

The application process is typically user-friendly and efficient. Applicants complete an online form, submit required documentation, and often receive a lending decision within a short period. Many online lenders utilise advanced algorithms and automated systems to assess creditworthiness, which can be advantageous for individuals with moderate or less-than-perfect credit histories.

As interest rates and associated costs can vary greatly from one lender to another, it’s wise for borrowers to compare a range of offers before committing. Tools such as loan comparison platforms and interest rate calculators can help borrowers understand the total repayment cost and make well-informed financial decisions.

The Benefits of Online Lenders

Online lenders have become a popular alternative to traditional banks, offering greater flexibility and convenience—especially for those who’ve been declined elsewhere.

- Faster application and approval process – Many online lenders provide instant decisions, with funds often paid out within hours or a couple of days. Ideal for urgent financial needs.

- More flexible lending criteria – Unlike traditional banks, online lenders may consider applicants with poor credit, irregular income, or limited credit history.

- Transparent comparisons – You can easily compare interest rates, fees, and repayment terms online, helping you make an informed choice without pressure.

- Convenient and paperless – Apply anytime, anywhere—no need for long queues or appointments. Most processes are completely digital.

- Regulated and trustworthy – Reputable online lenders are registered with the National Credit Regulator (NCR) in South Africa, ensuring they follow strict consumer protection laws.

Comparing Online Lenders and Traditional Banks

There are key differences between online lenders and conventional banks, particularly in how they operate and process loan applications. While traditional banks provide a broad range of financial services, including savings accounts, mortgages, and investment products, online lenders primarily specialise in offering loans, which often results in faster approvals and fewer eligibility requirements.

The main differences include:

| Feature | Online Lenders | Traditional Banks |

|---|---|---|

| Application Process | Fully digital, quick, no in-person visits required | Often requires paperwork and in-person visits |

| Approval Rates | More flexible criteria; higher approval rates | Stricter requirements; lower approval rates |

| Loan Focus | Primarily focused on loans | Offers a wide range of financial services beyond loans |

| Interest Rates & Fees | Can offer competitive rates; generally lower fees | May charge higher fees due to overhead and regulations |

| Speed of Processing | Faster approvals and fund disbursement | Slower processing and longer wait times |

| Accessibility | Available online 24/7 | Limited to branch hours and locations |

Understanding these distinctions allows borrowers to make informed financial decisions, ensuring they select the most suitable lending option based on their specific needs and circumstances.

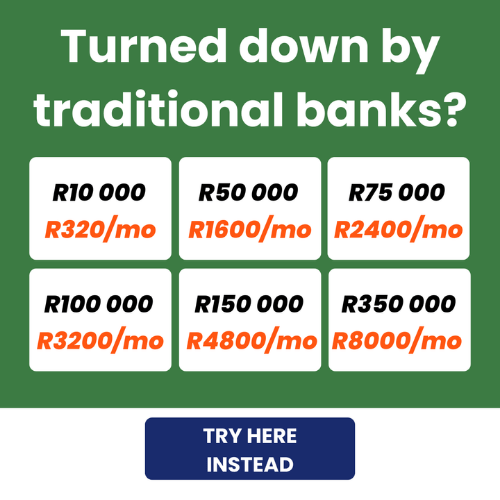

Been rejected more than once? Don’t lose hope. There are lenders who can help you secure a loan when all banks refuse, giving you a chance to move forward financially despite the rejections.

What is Arcadia Finance?

Arcadia Finance helps South Africans in the search for loans from different banks and lenders through our loan broker partners. We provide access to up to 19 reputable banks and lenders. By completing our loan application you will get multiple loan offers, which you can compare and select the most suitable offer. The service we offer is completely free of charge and you will not commit to anything by requesting for loan offers via Arcadia Finance. We only work with trusted loan brokers who collaborate with NCR licensed banks and lenders in South Africa.

Why Use Arcadia Finance?

- 100% free: The application is free and does not include any hidden fees.

- Quick & easy: The whole application process is done online in minutes.

- Convenient: Compare up to 19 banks & lenders with one application.

- Non-binding: You decide if you want to accept or decline your offers.

- Safe: Your personal data is safe with us.

Comparing Online Lenders in South Africa

When seeking a personal loan in South Africa, it’s essential to compare offerings from various online lenders to find the most suitable option for your financial needs. Below is an overview of several prominent online lending platforms:

| Lender | Loan Amounts | Repayment Terms | Key Features |

|---|---|---|---|

| MyLoan | Up to R350 000 | 2 – 72 months | Single application for multiple offers, no credit impact |

| Creditum | Dependent on lender | 2 – 72 months | NCR-licensed lenders, transparent process |

| Capfin | R1 000 – R50 000 | 6 – 24 months | No hidden fees, responsible lending |

| LendPlus | Varies based on assessment | Short-term (aligned with payday) | Fast payday loans, minimal documentation |

| Wonga | R500 – R8 000 | 4 days – 6 months | Fully online, no branch visits, quick approvals |

How to Choose a Trusted Online Lender

With so many online lenders available, it’s vital to choose one that’s both reputable and regulated. Here are a few key steps to help you make a confident and informed decision:

Look for NCR Registration in South Africa

Always ensure the lender is registered with the National Credit Regulator (NCR). This confirms that the lender complies with South Africa’s credit laws and consumer protection standards. You can verify registration directly on the NCR’s website.

Check Customer Reviews and Ratings

Take time to read customer feedback online. Reviews can provide valuable insight into a lender’s service quality, reliability, and how they handle complaints or issues. A consistently positive reputation is usually a good sign.

Compare Interest Rates and Fees

Not all loans are created equal. Compare the interest rates, service charges, and any additional fees across different lenders. Be cautious of hidden costs and always read the terms and conditions before committing to a loan.

The National Treasury encourages responsible borrowing and offers guidance on managing personal debt effectively in a volatile economy.

Conclusion

If your bank has declined your loan application, online lenders offer a practical alternative with faster approvals, flexible eligibility criteria, and fully digital application processes. However, it’s essential to compare different lenders, understand loan terms, and assess your financial situation before applying. By choosing the right lender and borrowing responsibly, you can access the funds you need while managing repayments effectively.

Frequently Asked Questions

Can I get a loan from an online lender if I have bad credit?

Yes, many online lenders have more flexible approval criteria than traditional banks. However, interest rates may be higher, and loan amounts could be lower for applicants with poor credit scores.

How long does it take to get approved for an online loan?

Most online lenders provide instant pre-approval or decisions within a few hours. Once approved, funds are typically disbursed within 24 to 48 hours, depending on the lender.

Are online loans safe to apply for in South Africa?

Yes, as long as you choose a registered and reputable lender. Ensure the lender is licensed by the National Credit Regulator (NCR) and avoid lenders that request upfront payments or have hidden fees.

What documents do I need to apply for an online loan?

Most online lenders require proof of identity (ID), proof of income (recent payslips or bank statements), and proof of residence. Some lenders may also request additional documents depending on the loan type.

How can I improve my chances of getting approved for a loan?

To increase approval chances, check your credit score, reduce existing debt, ensure your income meets the lender’s requirements, and submit complete and accurate documentation when applying.