If you are thinking about applying for a personal loan, you might be concerned that a poor credit history will affect your chances of being approved. This concern is understandable, but it should not prevent you from submitting an application. A low credit score can certainly make it more difficult to secure a personal loan. Nevertheless, approval is still possible. There are a number of lenders who are willing to assess applications from individuals with less-than-ideal credit records.

DISCLAIMER: The content of this article is based on publicly available information from the National Credit Act (NCA) as of the date of publication. Legal standards and interpretations may change, and the enforcement of specific provisions may vary depending on the circumstances.

Key Takeaways

- Low Credit Score Does Not Eliminate Loan Options: Even with a poor credit history, it is still possible to secure a loan in South Africa, though lenders may charge higher interest rates and apply stricter terms.

- Specialist Lenders And Alternatives Are Available: Borrowers with low credit scores can approach online lenders, credit-impaired providers, or opt for secured loans where collateral reduces the lender’s risk.

- Responsible Borrowing Can Improve Your Credit: Successfully repaying a loan, even one designed for bad credit, can gradually strengthen your credit score and improve future borrowing opportunities.

Credit Scoring In South Africa

A credit score refers to a numerical value, ranging from 0 to 1200 or 0 to 999 in South Africa, depending on the credit bureau. This figure assists lenders in evaluating an individual’s reliability when it comes to managing credit.

In simple terms, it is a number that financial institutions such as banks, retailers, and mobile service providers consult to decide how safe or risky it is to extend credit or loans to a person.

What Is A Good Credit Score?

In South Africa, a score of 650 or higher is generally seen as a good credit score, while anything above 700 is regarded as excellent.

A higher credit score indicates lower risk to lenders, which usually leads to better borrowing rates and reduced costs for individuals seeking credit. Maintaining a good credit score makes it far easier to secure loans, obtain credit cards, and even affects other aspects of financial well-being. It is worthwhile to consistently work towards improving your credit score over time.

What Is A Bad Credit Score?

A credit score below 550 is considered poor in South Africa. While different credit providers might have slight variations in their thresholds, falling below 550 typically places a person in a high-risk category.

Those with lower scores often face difficulty obtaining credit or loan approvals. In most cases, individuals with bad credit scores encounter high-interest rates, more stringent loan terms, or outright rejection by lenders.

Rebuilding your financial credibility starts with a few strategic moves. Discover practical steps to improve your credit score that can pave the way for better interest rates and improved loan offers down the line. Whether it’s disputing errors or paying off lingering debts, this guide is your action plan.

DISCLAIMER: Readers should exercise caution and conduct their own research before entering into any loan agreement. It is recommended to review all loan terms and conditions carefully and seek independent financial advice where necessary.

What Can Damage Your Credit Score

- Late Payments: Always maintain a consistent payment routine to avoid missing due dates.

- High Debt Levels: Limiting the number of active credit accounts helps to prevent excessive debt accumulation.

- Exceeding Credit Card Limits: Spending beyond your credit card limit may indicate overdependence on borrowed funds.

- Hard Credit Enquiries: Lenders’ hard checks can lower your credit score and remain visible on your credit report for an extended period. Consider whether applying for new credit is truly necessary.

- Frequent Account Changes: Opening or closing credit accounts may cause a temporary decrease in your credit score, though it is usually possible to recover over time.

Who Calculates Your Credit Score?

Your credit score is determined by a credit bureau. In South Africa, there are four major credit bureaus responsible for this process: Experian, TransUnion, Compuscan, and XDS. These credit bureaus receive regular updates from lenders regarding the credit accounts you hold and how responsibly you manage your repayments. Information such as court judgments issued against you or whether you are currently under debt review is also provided to the credit bureaus. All of these details are compiled into your credit report, which serves as the basis for calculating your credit score.

About Arcadia Finance

Secure your loan with ease through Arcadia Finance. With no application fees and access to 19 carefully vetted lenders, all fully registered with South Africa’s National Credit Regulator, you can count on a seamless, trustworthy borrowing experience. Find a loan that fits your needs with confidence.

Can I Get A Loan With A Low Credit Score

It is possible to obtain a personal loan even if you have a low credit score. Some lenders specialise in providing loans to individuals with poor credit histories. However, these loans usually come with higher interest rates, as lenders view lending to individuals with lower credit scores as a greater risk. When assessing your loan application, these lenders will place a strong emphasis on your current income and your capacity to meet the repayment obligations, rather than focusing solely on your past credit behaviour.

Understanding Loan Options With A Low Credit Score

Traditional Banks

Securing a loan from a traditional bank can be more difficult if your credit score is low, as these institutions generally apply stricter approval standards. That said, obtaining a loan is still possible in some cases, especially if you have an established account history or can offer collateral to reduce the lender’s risk.

Online Lending Platforms

Online lenders, including peer-to-peer services and non-bank financial providers, are often more open to working with individuals who have lower credit scores. These lenders usually take a broader view by assessing your income, employment record, and other financial indicators alongside your credit rating before making a decision.

Credit-Impaired Loan Providers

Certain financial institutions focus on offering loans specifically to people who have poor credit or limited credit history. These lenders generally charge higher interest rates and administrative fees, but they can offer an option when mainstream banks are not viable.

Loans Secured By Assets

If you have a low credit score, applying for a secured loan may be more practical. This type of loan requires an asset—such as a car or fixed deposit—to act as collateral. Since the lender has a safeguard in place, they may be more open to granting credit, even if your credit report reflects past challenges.

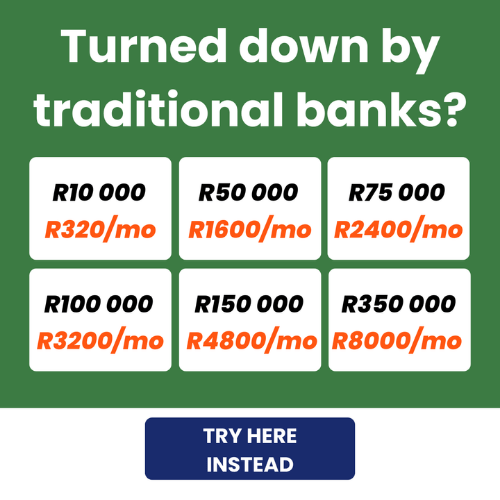

Comparison of Lenders for Low Credit Score Loans in South Africa

| Lender/Platform | Loan Amount Range | Repayment Terms | Interest Rates | Key Features |

|---|---|---|---|---|

| African Bank | R2 000 – R500 000 | 7 – 72 months | From 5% to 28% | Offers fixed-interest-rate loans; no penalties for early settlement; requires proof of income and bank statements. |

| Old Mutual | R2 000 – R250 000 | 3 – 72 months | Up to 29.25% | Fixed interest rates; quick online application; funds disbursed within 24 hours upon approval. |

| Standard Bank | R3 000 – R300 000 | 12 – 72 months | Personalised rates | Apply online or via app; flexible repayment terms; use rewards points to pay off loan. |

| SupaSmartLoans | R1 000 – R200 000 | Varies | Varies | Broker service that matches applicants with lenders; quick application process; caters to various credit profiles. |

| Hoopla Loans | R100 – R250 000 | 3 – 60 months | Varies | Works with a panel of lenders; considers bad credit histories; 100% online application; potential same-day funding. |

DISCLAIMER: Arcadia Finance accepts no liability for any financial loss, damage, or inconvenience that may result from the use of this information or from engagements with any listed lenders or third-party providers.

A Loan For Bad Credit Could Help Or Harm Your Credit Rating

Taking out a loan designed for bad credit and successfully repaying it on time and in full can positively influence your credit rating. It demonstrates to lenders that you are capable of managing debt responsibly and meeting your financial obligations. This record of reliable repayment could make it easier for you to access future loans, possibly at a more favourable interest rate.

However, if you obtain a loan for bad credit and fail to keep up with your repayments, it may cause greater harm to your credit score than defaulting on a standard loan. This type of damage can seriously limit your ability to secure credit later on, making future borrowing much more difficult.

Struggling with scattered debt? A smart way to regain control is by exploring debt consolidation loans. These allow you to combine multiple obligations into one manageable payment—often with better terms than your current commitments.

Pros and Cons of Low Credit Score Loans

Bad credit loans can offer a helpful solution when traditional lending isn’t an option. However, they come with both advantages and disadvantages worth considering:

Pros of Low Credit Score Loans

- Access to Finance: Even with a poor credit rating, you may still be eligible for a loan, which can help cover urgent expenses or consolidate existing debts.

- Credit Rebuilding Opportunity: Making regular, on-time repayments can improve your credit score over time, opening the door to better financial options.

- Flexible Lender Options: Alternative lenders often consider more than just your credit score, such as employment status and income consistency.

- Quick Approval Times: Many bad credit loans feature fast online applications and, in some cases, same-day payouts.

Cons of Low Credit Score Loans

- Higher Interest Rates: These loans typically come with higher interest rates, making them more expensive in the long term.

- Fees and Charges: Some lenders may include additional costs such as application fees, late payment penalties, or early settlement fees.

- Risk of Falling into Debt: If not carefully managed, borrowing can become a cycle—especially if you’re using loans to cover other debt.

- Limited Loan Amounts and Terms: You may only qualify for lower loan amounts or shorter repayment periods compared to borrowers with stronger credit profiles.

DISCLAIMER: Arcadia Finance is not a lender and does not provide personal loans directly. The information provided in this article is for general informational purposes only and should not be considered financial advice, loan advice, or credit counselling.

Tips To Improve Your Credit Score

If you currently have a low credit score, there is positive news – there are several steps you can take to raise it, and improvements may become visible sooner than expected through consistent good habits.

In general, you can improve your credit score by following these practices:

- Pay Your Bills Promptly: Make sure that you pay all your bills by their due dates to build a record of timely payments.

- Settle The Full Outstanding Balance Each Month: Whenever possible, pay off the full amount owed on your credit accounts rather than just the minimum instalments.

- Commit To Meeting Minimum Repayment Requirements: Before taking out any loan or credit facility, ensure that you can consistently meet at least the minimum monthly repayment amount.

- Limit Your Use Of Available Credit: Aim to use no more than 30% of your total credit limit across your accounts. This helps to demonstrate responsible management of credit.

Your credit score essentially mirrors your borrowing behaviour. Maintaining good habits over time remains the most reliable way to sustain a strong credit rating. It is also advisable to review your credit report at least twice a year to check for any inaccuracies or any signs of possible identity fraud.

By establishing responsible financial habits and monitoring your records carefully, you can steadily build and preserve a healthy credit profile, which will serve you well when applying for future credit or loans.

Conclusion

Although a low credit score can create challenges when seeking a personal loan in South Africa, it does not mean that approval is impossible. Various lenders offer products tailored to individuals with less-than-perfect credit histories, although these often come with higher costs. By carefully selecting loan options, maintaining responsible borrowing habits, and taking steps to improve your credit score over time, you can gradually rebuild your financial standing and access more favourable credit opportunities in the future.

Frequently Asked Questions

Can I Get A Loan If I Have A Bad Credit Score?

Yes, it is possible to obtain a loan even with a poor credit score. Some lenders specialise in working with individuals who have low credit ratings, although you should be prepared for higher interest rates and stricter lending conditions compared to those with good credit.

What Interest Rates Should I Expect With A Low Credit Score?

If you have a low credit score, you are likely to face higher interest rates than borrowers with strong credit profiles. Lenders charge more to offset the greater risk associated with lending to someone who has a history of credit difficulties.

Will Paying Off A Loan Improve My Credit Score?

Successfully paying off a loan according to the agreed repayment schedule can have a positive effect on your credit score. It shows lenders that you are capable of managing debt responsibly and meeting your financial commitments on time.

Are Secured Loans A Good Option For Poor Credit?

Secured loans can often be a more accessible option for borrowers with poor credit, as offering an asset like a car or savings as collateral reduces the lender’s risk. This can make approval more likely and sometimes help secure better loan terms.

How Can I Quickly Improve My Credit Score?

To start improving your credit score, focus on paying all bills and instalments on time, reducing your outstanding debts, keeping your use of available credit low, and reviewing your credit report regularly to correct any errors that may be affecting your rating.