Accessible and Affordable Micro Loans for All

Need Quick Cash? Find Out How Micro Loans Work!

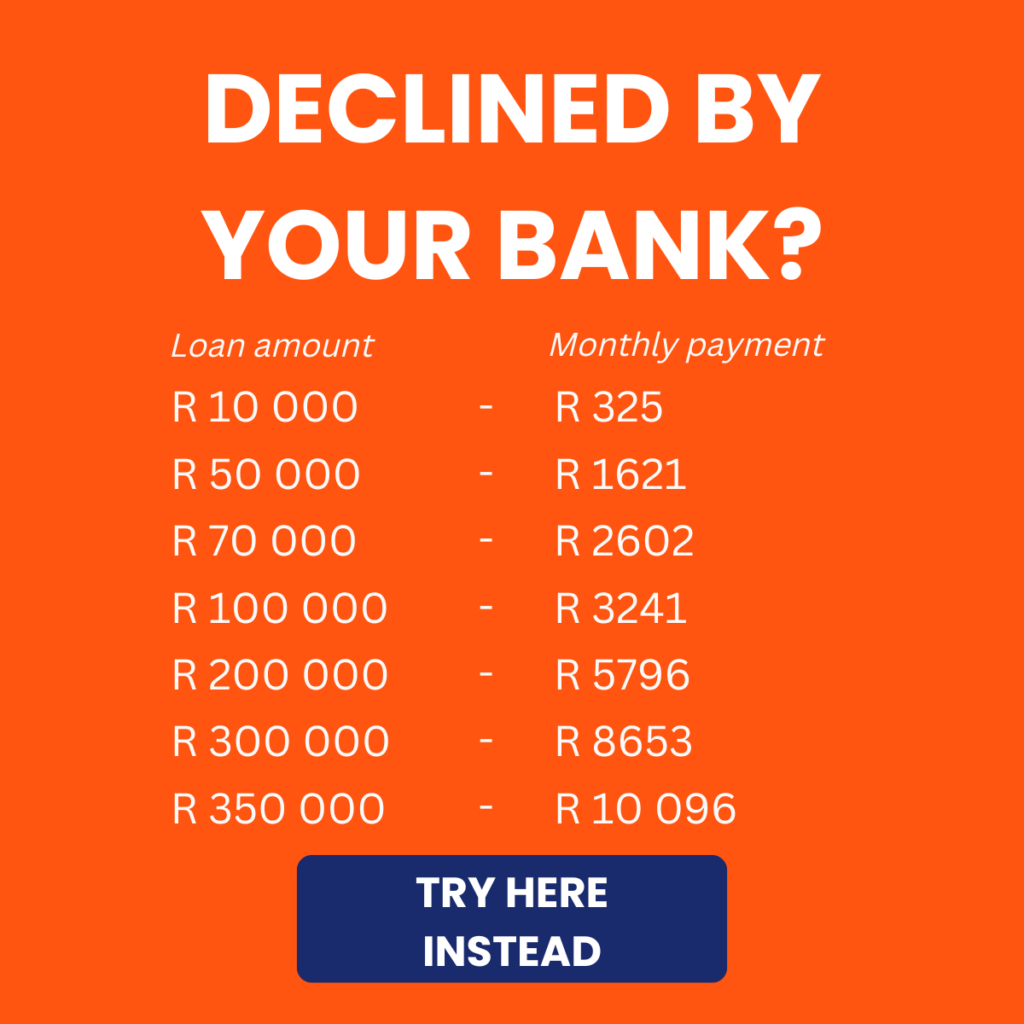

Arcadia Finance helps you in the search of loans from different banks and lenders. Fill in a free application and get loan offers from up to 16 lenders. We work with well-known, trusted, and NCR-licensed lenders in South Africa.

What are Micro Loans?

Micro loans are small, short-term loans specifically designed to assist individuals or small businesses that may lack access to traditional financial services. These loans primarily target entrepreneurs, start-ups, and low-income individuals, enabling them to fund small-scale ventures or address immediate financial needs. Common uses for micro loans include purchasing inventory, acquiring equipment, or covering operational costs.

Typically, micro loans range from a few hundred to a few thousand South African Rand, making them accessible to those without a credit history or collateral. They are offered by microfinance institutions, non-profit organisations, and, in some cases, government agencies or banks. The primary aim of micro loans is to promote financial inclusion and economic development by empowering small-scale entrepreneurs to achieve self-sufficiency.

About Arcadia Finance

Get your loan smoothly and confidently with Arcadia Finance. Take advantage of zero application fees and access 16 trusted lenders, each adhering to South Africa’s National Credit Regulator requirements. Experience a fast, reliable process designed with your financial goals in mind.

Types of Micro Loans Available in South Africa

Short-Term Personal Micro Loans

Short-term personal micro loans are designed for immediate, often unexpected personal expenses. These unsecured loans do not require collateral and typically have terms ranging from a few weeks to a few months. South Africans commonly use them for costs such as medical bills, home repairs, or education fees. Due to their shorter terms, these loans often carry higher interest rates than traditional loans, so borrowers should ensure they can meet the repayment schedule.

Business Micro Loans for Entrepreneurs

Business micro loans provide essential support to small-scale entrepreneurs seeking capital to start or grow their businesses. They are particularly valuable for individuals in informal sectors or those unable to meet the requirements for traditional business loans. These loans can finance inventory purchases, operational costs, or business improvements, often featuring flexible repayment terms tailored to the borrower’s cash flow. Additionally, some lenders offer mentorship or business development support to promote sustainability.

Emergency Micro Loans

Emergency micro loans are intended for urgent, unforeseen expenses, providing quick access to funds. South Africans frequently use these loans for unexpected costs such as medical emergencies or urgent repairs. They can be granted within hours of application, making them useful in crisis situations. However, interest rates on these loans are often higher, and repayment periods are shorter. Borrowers should assess their repayment ability before opting for this type of loan.

Payday Micro Loans

Payday micro loans help cover expenses until the borrower’s next payday, making them ideal for temporary cash shortages. These short-term loans typically require repayment within 30 days. While they offer quick solutions, they can carry high interest rates and fees. Borrowers are advised to use payday loans sparingly to avoid falling into a cycle of debt.

Agricultural Micro Loans for Rural Communities

Agricultural micro loans are tailored for South Africa’s rural communities, where farming is a primary source of income. These loans provide small-scale farmers with funds for seeds, fertiliser, equipment, and other essential resources. They play a vital role in supporting food production and economic growth in rural areas. Repayment terms are often aligned with the seasonal nature of farming, allowing flexibility post-harvest. Some lenders may also offer technical support or training to help farmers improve productivity and effectively manage their loans.

Eligibility Criteria and Documentation for Micro Loans in South Africa

To qualify for a micro loan in South Africa, borrowers typically need to meet the following requirements:

- Age: Applicants must be at least 18 years old to legally enter into a financial agreement.

- South African ID: Proof of citizenship or residency is required for identity verification.

- Steady Income: Borrowers must demonstrate a reliable income from employment, self-employment, or social grants to assure lenders of their repayment ability.

- Active Bank Account: An active bank account is necessary for loan disbursement and repayment.

Some lenders may also set a minimum income requirement depending on their policies and the loan amount.

Required Documentation

Applicants usually need to provide the following documentation:

- ID: A valid South African ID for identity verification.

- Proof of Income: Recent payslips, bank statements, or a letter from an employer confirming income.

- Bank Statements: At least three months of bank statements to assess financial habits.

- Proof of Address: Utility bills or lease agreements that confirm residency.

- Credit History: While some lenders check credit records, many accept applicants with little or no credit history.

Application Process for Micro Loans

Applying for a micro loan in South Africa is generally straightforward, but understanding the steps and potential pitfalls can enhance the experience. Many lenders, including banks, financial institutions, and fintech platforms, offer simplified application processes, especially with the rise of digital options.

- Initial Consultation and Pre-Qualification

The process begins with a pre-qualification where lenders assess eligibility based on factors such as income, desired loan amount, and purpose, usually without conducting a hard credit check. Digital platforms often provide quick eligibility assessments.

- Submitting an Application

After pre-qualification, applicants submit a full application along with necessary documents, including identification, proof of income, and bank statements. Applications can be made online or via mobile apps for convenience; however, traditional lenders may require in-person submissions. Accuracy is crucial to avoid delays.

- Approval and Disbursement Timeline

Once submitted, lenders review the application, which may include a credit check. Approval times vary, but micro loans are typically approved quickly, especially through digital channels. Some lenders can disburse funds within hours, while traditional lenders may take a few days. Approved funds are deposited directly into the applicant’s bank account for urgent needs.

Common Pitfalls

While the application process for micro loans is generally simple, applicants should be aware of common pitfalls:

- Incomplete or Incorrect Documentation: Missing or inaccurate documents can lead to delays or rejection. Borrowers should verify all required documents for accuracy to prevent complications.

- Requesting Unnecessary Loan Amounts: Only borrow what is needed, as larger loans increase monthly repayment burdens and financial stress due to higher interest rates.

- Unclear Repayment Terms: Carefully read the repayment terms, including interest rates, fees, and penalties, to avoid misunderstandings and unexpected costs.

- Multiple Applications: Applying for multiple loans in a short time can negatively impact credit scores and reduce approval chances. Focus on one lender at a time to maintain a positive credit profile.

To avoid these pitfalls, applicants should research lenders thoroughly, prepare documentation in advance, and understand all terms before applying.

Interest Rates and Fees

Micro loan interest rates are generally higher than those for traditional loans due to their unsecured nature and shorter repayment terms. These rates reflect the higher risk for lenders, particularly for borrowers with limited credit history. In South Africa, while micro loan rates are regulated, they can vary significantly among lenders. Rates are typically expressed as monthly or annual percentages, with smaller loans often attracting higher rates because of their shorter terms.

Breakdown of Typical Fees

Micro loans usually come with additional fees that can increase the overall cost of borrowing. Common fees include:

- Initiation Fee: A one-time charge at the start of the loan to cover processing costs, typically calculated as a percentage of the loan amount and sometimes capped by regulations.

- Monthly Service Fee: An ongoing fee throughout the loan term to cover administrative costs, usually added to the repayment amount.

- Early Settlement Fee: Some lenders charge a fee for early repayment; however, this is not universal. Borrowers should confirm if this applies.

- Late Payment Fee: Charged if a scheduled payment is missed, potentially increasing overall debt and negatively impacting credit scores.

Factors Influencing Interest Rates

Several factors affect the interest rate offered to borrowers:

- Credit Score: Borrowers with strong credit histories typically receive lower rates, while those with poor or limited credit may face higher rates.

- Loan Term: Shorter-term loans usually carry higher monthly rates compared to longer-term options, as lenders seek quicker returns.

- Loan Amount: Larger loans may have lower rates compared to smaller ones, as the risk is spread over a larger amount.

- Lender Type: Traditional lenders often provide slightly lower rates than online or payday lenders, although this varies by lender.

Repayment Options and Terms

Repayment terms for micro loans vary by lender and loan type, typically offering flexible structures for weekly or monthly repayments based on borrowers’ preferences. Weekly payments are often suited for individuals with regular weekly income, while monthly payments tend to be more beneficial for salaried employees. Repayment schedules are set during the application process to ensure clarity on the borrower’s obligations.

Many lenders allow early repayment, which can help borrowers save on interest. However, it’s essential for borrowers to verify whether any early settlement fees apply.

Missing payments can lead to penalties; most lenders impose a late payment fee that adds to the outstanding balance. Repeated missed payments may result in higher fees, legal action, and a negative impact on the borrower’s credit score. Persistent defaults can trigger collections, further adding to financial stress.

Case Examples of Repayment Terms

Consider the following examples to illustrate repayment terms:

- Weekly Payment Example: A borrower takes a R1 000 micro loan with a six-week term. The weekly repayment amount, including interest and fees, is R200. Over six weeks, the total repayment comes to R1 200.

- Monthly Payment Example: A borrower takes a R2 000 loan with a three-month term. The monthly repayment, including fees and interest, is R750. At the end of three months, the total repayment amounts to R2 250.

Pros and Cons of Micro Loans

Micro loans can be a valuable financial resource for individuals and small businesses in South Africa. While they offer several benefits, they also come with potential drawbacks.

Pros

- Quick Access to Funds: Micro loans are often approved and disbursed rapidly, providing borrowers with immediate cash for urgent needs.

- Flexible Eligibility Criteria: Many lenders have more relaxed requirements, making it easier for individuals with limited credit history to qualify.

- Small Loan Amounts: Ideal for those needing a small amount of money for personal expenses or to fund a small business.

- Support for Entrepreneurs: Business micro loans can provide crucial funding for small business owners, helping to stimulate economic growth.

- Quick Application Process: Many lenders offer online applications that are easy to complete, often resulting in rapid approvals.

Cons

- High Interest Rates: Micro loans typically have higher interest rates compared to traditional loans, which can increase the total cost of borrowing.

- Short Repayment Terms: Repayment periods are usually short, which may strain borrowers who are not prepared for frequent payments.

- Risk of Debt Cycle: Borrowers may find themselves taking out multiple loans to cover expenses, leading to a cycle of debt.

- Fees and Charges: In addition to interest, borrowers may face various fees (e.g., initiation, service fees) that can add to the overall cost of the loan.

- Limited Loan Amounts: Micro loans may not be sufficient for larger financial needs, limiting their usefulness for significant investments.

Micro Loans vs Other Loan Types

When considering financing options, it’s essential to compare micro loans with other types of loans, such as personal loans, payday loans, and credit cards.

| Loan Type | Overview | Pros | Cons |

|---|---|---|---|

| Micro Loans | Small, short-term loans for urgent needs. | Quick access, flexible eligibility. | High-interest rates, short repayment terms. |

| Personal Loans | Larger loans with fixed terms and lower rates. | Lower interest rates, longer repayment. | Stricter eligibility, longer approval time. |

| Payday Loans | Short-term loans typically due on the next payday. | Fast approval, immediate cash. | Extremely high rates, risk of debt cycle. |

| Credit Cards | Revolving credit that can be used as needed. | Flexible spending, rewards programs. | High-interest rates if not paid in full. |

Conclusion

Micro loans serve as a vital financial resource for South Africans seeking quick access to funds for personal emergencies or small business needs. With various options available—including short-term personal loans, business loans, and emergency micro loans—these financial products offer flexibility and accessibility for those who may struggle with traditional lending requirements.

Frequently Asked Questions

Micro loans are small, short-term loans designed to assist individuals or small businesses in meeting immediate financial needs, typically ranging from a few hundred to several thousand rand.

Eligibility criteria vary by lender but generally include being at least 18 years old, possessing a valid South African ID, providing proof of a steady income, and maintaining an active bank account. Some lenders may also consider your credit history.

Available types include short-term personal loans, business micro loans, emergency loans, payday loans, and agricultural loans, each catering to specific financial circumstances.

Interest rates for micro loans are typically higher than those for traditional loans due to their unsecured nature. Common fees include initiation fees, monthly service fees, and late payment fees, so borrowers should review the terms carefully before applying.

Applications can be submitted online or through mobile apps, beginning with a pre-qualification process followed by a full application that requires documentation such as an ID, proof of income, and bank statements. Approval times can vary, with some lenders disbursing funds within hours.